For years, European investors have poured billions into “sustainable” mutual funds, trusting that their capital was driving positive change. The promise was simple: by choosing an Environmental, Social, and Governance (ESG) fund, you were divesting from fossil fuels and supporting ethical labour practices.

However, as we move through 2025, a harsh reality is coming to light. Despite the “green” labels, many of these funds remain heavily exposed to the very industries they claim to exclude. From coal-fired power plants hidden in complex supply chains to child labour in mineral extraction, the dirty secret of ESG funds is that, for too long, they have relied on vague narratives rather than hard data.

But the era of ambiguity is ending. With the enforcement of the Corporate Sustainability Reporting Directive (CSRD), the European Sustainability Reporting Standards (ESRS), and the Sustainable Finance Disclosure Regulation (SFDR), the regulatory landscape is forcing a paradigm shift from voluntary storytelling to mandatory, auditable evidence.

Until recently, the definition of a “sustainable investment” was largely left to asset managers. Without a standardized rulebook, a fund could exclude tobacco companies but still invest in oil majors “transitioning” to green energy, or tech giants relying on conflict minerals.

This disconnect stemmed from a lack of reliable data. Corporate sustainability disclosure was often voluntary and narrative-based, allowing companies to cherry-pick their achievements while ignoring systemic risks. However, the European Union has rolled out a comprehensive sustainable finance framework designed to reorient capital flows towards genuinely sustainable activities. This ecosystem relies on three pillars: CSRD, EU Taxonomy, and SFDR

To clean up the investment landscape, regulators first had to define what “green” actually means.

1. The Sustainable Finance Disclosure Regulation (SFDR)

The SFDR imposes transparency requirements on Financial Market Participants (FMPs), such as asset managers and pension funds. It categorizes funds into three distinct buckets to prevent mislabelling.

Article 6 Funds: Funds that do not integrate sustainability into their investment process.

Article 8 Funds (“Light Green”): Funds that promote environmental or social characteristics.

Article 9 Funds (“Dark Green”): Funds that have sustainable investment as their specific objective.

Crucially, FMPs must now report on Principal Adverse Impacts (PAIs)—the most significant negative impacts of their investments on factors like greenhouse gas (GHG) emissions and human rights violations. This requirement makes it increasingly difficult for a fund to claim “sustainability” while ignoring the carbon footprint of its portfolio.

If SFDR is the label, the EU Taxonomy is the dictionary. It is a classification system that establishes a common definition for environmentally sustainable economic activities. For an activity—and by extension, a fund investing in it—to be Taxonomy-aligned, it must meet three strict criteria:

Substantial Contribution: It must significantly contribute to at least one of six environmental objectives (e.g., climate change mitigation).

Do No Significant Harm (DNSH): It cannot harm any of the other five objectives.

Minimum Social Safeguards: It must comply with international human rights standards, such as the OECD Guidelines for Multinational Enterprises.

This third criterion is the “poison pill” for dirty funds. A solar panel manufacturer might pass the environmental test, but if their supply chain is tainted by forced labour, they fail the Taxonomy alignment test entirely.

The Data Revolution: CSRD and ESRS

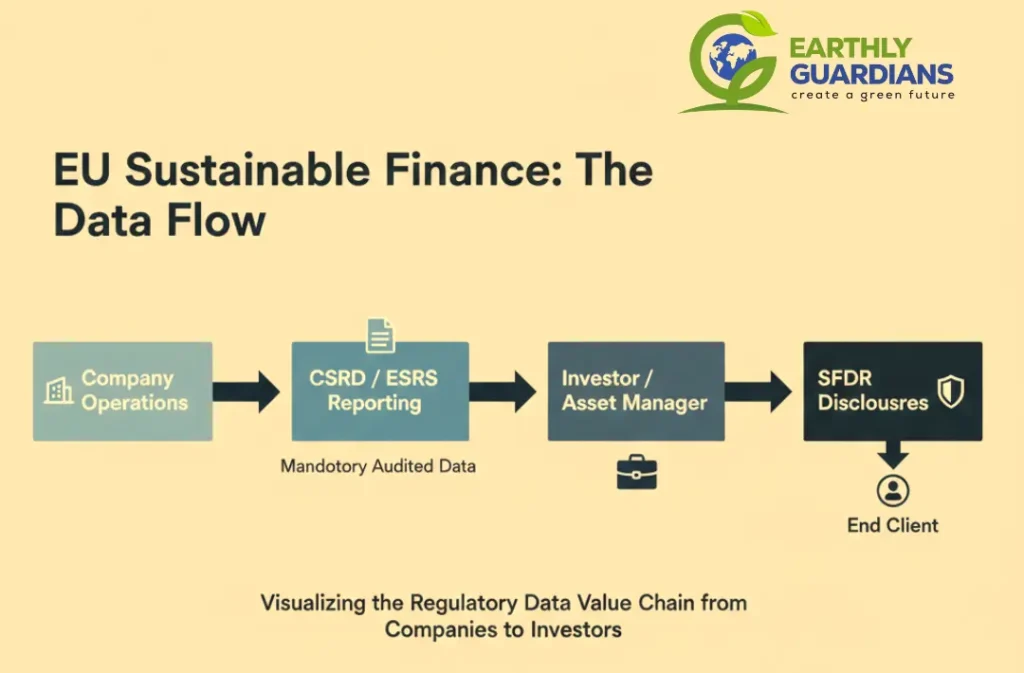

While SFDR and the EU Taxonomy set the rules for investors, they depend entirely on data coming from companies. This is where the Corporate Sustainability Reporting Directive (CSRD) changes the game.

Replacing the older Non-Financial Reporting Directive (NFRD), the CSRD mandates that large EU and listed companies report under the detailed European Sustainability Reporting Standards (ESRS). This creates a direct “data value chain”: companies report audited data under CSRD, which investors then use to justify their SFDR classifications.

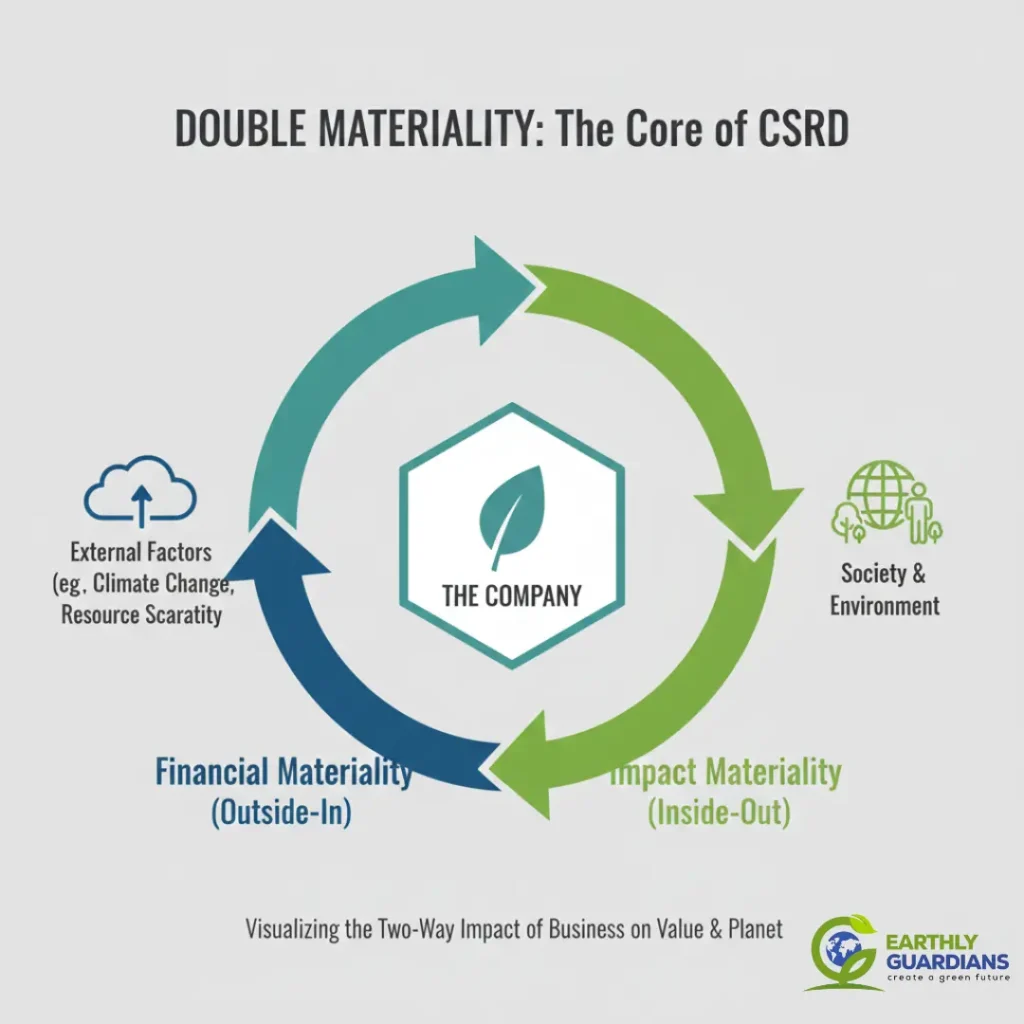

Double Materiality: No More Hiding

The cornerstone of CSRD is Double Materiality. Companies can no longer just report on how climate change affects their profits (Financial Materiality). They must also report on their Impact Materiality—how their operations impact people and the environment.

Financial Materiality (Outside-In): Aligns with IFRS S1 and S2 standards, focusing on enterprise value for investors.

Impact Materiality (Inside-Out): Aligns with GRI Standards, focusing on impacts on the economy, environment, and people.

This mandatory dual perspective ensures that a mining company cannot simply report on “regulatory risks” while ignoring the deforestation caused by its new mine.

Exposing the Hidden Risks: Coal, Labour, and Deforestation

How exactly do these new standards expose the “dirty secrets” of coal, child labour, and deforestation?

1. Coal and Carbon: Scope 3 and Transition Plans

Under ESRS E1 (Climate Change), companies must disclose their gross Scope 1, 2, and 3 GHG emissions. Scope 3 is critical because it covers the value chain—often accounting for over 80% of a company’s footprint. Furthermore, companies must publish a climate transition plan aligned with the Paris Agreement (1.5°C goal). They must quantify the CapEx and OpEx allocated to this transition. If an “ESG” fund holds a utility company that has no credible plan to phase out coal, the Taxonomy alignment data will reveal a 0% alignment for those activities, forcing the fund manager to explain the discrepancy.

2. Child Labour: The Social Supply Chain

Child labour is often buried deep in the supply chain (Scope 3). ESRS S2 (Workers in the Value Chain) requires companies to disclose their due diligence processes for identifying and managing risks like child labour and inadequate wages among suppliers. Additionally, the GRI Standards work in tandem here. The interoperability between GRI and ESRS means that companies using GRI for impact reporting are well-positioned to meet the “Impact Materiality” requirements of CSRD. If a company fails to map its supply chain risks, it faces compliance failure; if it does map them and finds violations, it must report them.

3. Deforestation: Biodiversity Standards

Deforestation is addressed under ESRS E4 (Biodiversity and Ecosystems). This standard requires companies to report on their impacts and dependencies on nature, including the location of sites in biodiversity-sensitive areas. It aligns with the Taskforce on Nature-related Financial Disclosures (TNFD) framework. An ESG fund investing in an agricultural giant now has to look for specific disclosures on land-use change and “no net loss” commitments, rather than relying on a vague “earth-friendly” branding.

The Role of Assurance: Trust, but Verify

Perhaps the most significant change in 2025 is mandatory assurance. CSRD requires that sustainability information be subjected to limited assurance by an independent third party, with a roadmap to reasonable assurance (audit-grade) in the future.

This elevates ESG data from a marketing exercise to a finance-grade process. The data must be digitally tagged in XBRL format, making it machine-readable and comparable across thousands of companies. Investors can no longer plead ignorance; the data is standardized, audited, and digital.

Conclusion: A New Era for Investor Trust

The “dirty secret” of ESG funds—their historical ability to hide toxic assets behind green labels—is being dismantled by regulation. The combination of CSRD, ESRS, SFDR, and the EU Taxonomy has created a self-reinforcing ecosystem of transparency.

For European SMEs and large corporates, this means that access to capital is now directly linked to data quality. Investors managing Article 8 and Article 9 funds are desperate for high-quality, Taxonomy-aligned assets to fulfill their own reporting obligations. Companies that can provide transparent, assured data on their supply chains and carbon footprints will attract lower-cost capital and build lasting investor trust.

The days of “trust me, we’re green” are over. In 2025, the market demands: “Show me the data.”

Partner with Earthly Guardians

Navigating the complex landscape of CSRD, SFDR, and EU Taxonomy requires more than just good intentions; it requires technical expertise. Partner with Earthly Guardians to build a robust ESG reporting framework, ensure your data is audit-ready, and make your operations genuinely sustainable. Let’s turn your compliance burden into a competitive advantage.