The year is 2025. Global markets have never been more volatile, climate lawsuits are at an all-time high, and institutional investors manage more than $50 trillion in ESG-labeled assets. Yet, when you peel back the glossy sustainability reports, one uncomfortable truth remains: the vast majority of large corporations are still not taking ESG seriously.

They are not ignorant. They are not short-sighted in the traditional sense. They are calculating — coldly, rationally, and correctly — that the cost of genuine ESG transformation far outweighs the current punishment for faking it.

This is not cynicism. This is arithmetic.

- The Punishment Gap is Still Massive

In 2023, a company paid $4.3 billion for Dieselgate. In 2024, the combined fines for greenwashing and ESG-related misreporting across the entire S&P 500 did not cross $600 million. Do the math. A company can spend $500 million on greenwashing campaigns, get caught, pay a $50–150 million fine (often settled without admission of guilt), and still come out ahead versus spending $5–15 billion on actual decarbonization of supply chains.

The SEC’s climate disclosure rule (finally passed in watered-down form in 2024) is toothless. Scope 3 is voluntary. Materiality thresholds are vague. European CSRD is stricter, but enforcement is still years behind. The largest fine under CSDDD so far? €18 million against a fashion retailer. That is less than what some CEOs make in a single year.

Until the punishment for lying exceeds the cost of compliance by an order of magnitude, rational actors will keep lying.

- The Investor Incentive Mirage

A famous company’s manager stopped using the word “ESG” in his 2024 annual letter. Why? Because Republican states pulled $15 billion from the firm. The anti-ESG backlash in the US worked. Net flows into sustainable funds turned negative in 2023–2024 for the first time since tracking began.

Universal owners own ~20–25% of most S&P 500 companies. They should, in theory, push for system-level change. But their own business model depends on low fees, which means they cannot afford to lose mandates from red-state pension funds. So they vote with management 92–95% of the time on climate resolutions (ISS data 2024).

Result? The largest pools of capital in human history are structurally incapable of enforcing the change they publicly demand.

- The C-Suite Compensation Trap

In 2024, only 19% of CEO pay in the Russell 3000 was tied to any ESG metric (FW Cook study). Even when it is tied, the weight is usually 10–15%, and the targets are laughably easy (“achieve 2019-level emissions by 2030” while business grows 40%).

Compare this to revenue or EPS targets that carry 60–70% weight. A CEO who sacrifices 2–3% near-term margin to decarbonize will miss bonus targets and get fired within 24 months. A CEO who greenwashes aggressively keeps the job, the bonus, and the stock awards.

This is not moral failure. This is game theory working exactly as designed.

- The Middle Management Meat Grinder

Even when the CEO genuinely wants to change, the machinery of the corporation fights back. I have spoken to sustainability heads of three Fortune-100 companies in the last six months. All three said the same thing privately:

“My budget gets cut every time oil drops below $70 or when China floods the market with cheap solar/EV components. My boss supports me in public, but when push comes to shove, the business unit leaders win because they control profit, and I control PowerPoint slides.”

ESG teams remain cost centers. Procurement, operations, and manufacturing remain profit centers. Guess who wins internal battles?

- The “We Are Already Doing A Lot” Delusion

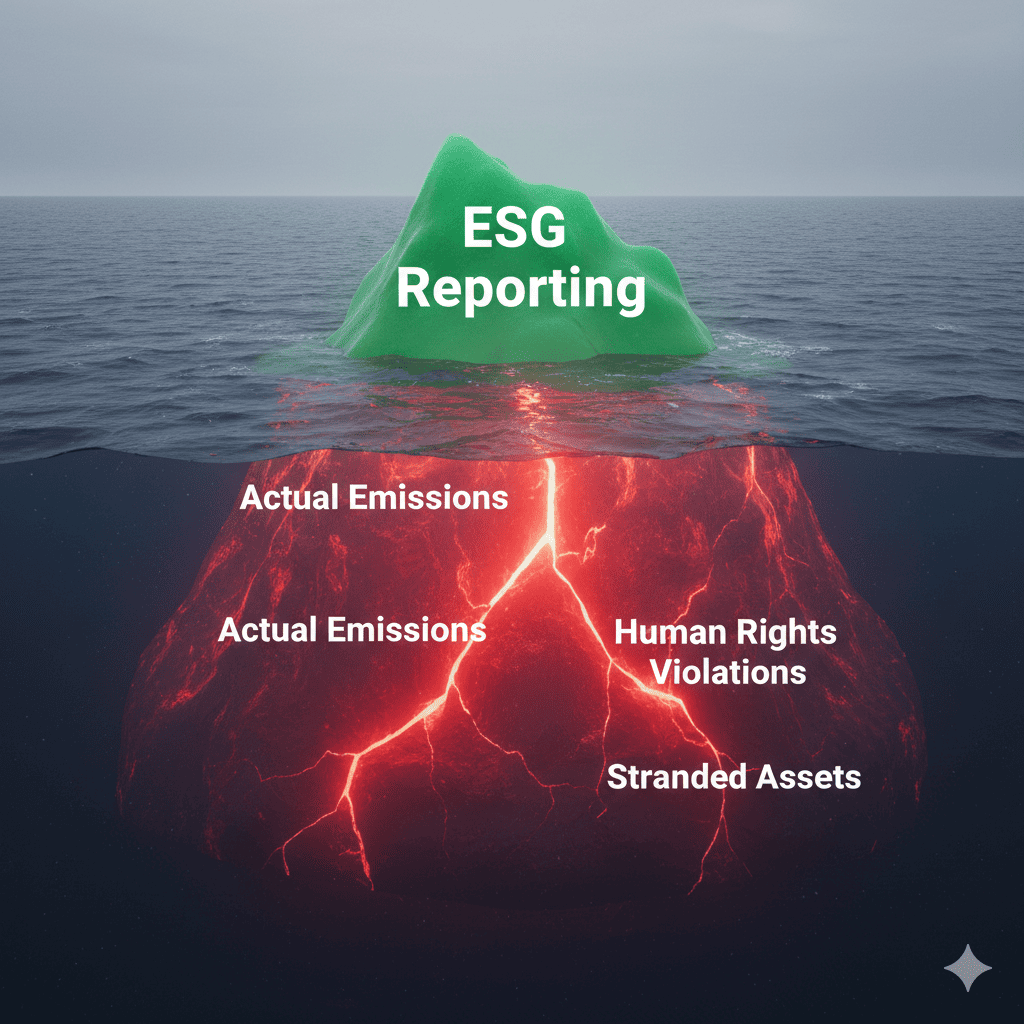

A very famous tech company emitted 14.3 million tCO₂e in 2023 while claiming to be carbon neutral (via offsets). A prominent ecommerce company’s emissions rose 34% from 2019–2023 while it became the world’s largest buyer of renewable energy. Apple’s suppliers in China still run mostly on coal, but the iPhone box says “100% clean energy”.

These are not bad companies. These are honest representations of how broken the current accounting rules are. Every tech giant can claim “net zero” while its value chain spews carbon, because offsets are cheap and Scope 3 is optional.

The bar is so low that being slightly better than average feels like leadership.

- The Regulatory Fragmentation Bonus

Companies operate in 195 countries with different rules. CSRD in Europe, SEC in America (weak), ISSB globally (voluntary), India’s BRSR, China’s green taxonomy — none align perfectly. A truly global company can choose the most convenient reporting jurisdiction for each entity and still comply with local laws.

This is not a bug. For multinational tax lawyers and sustainability consultants, this is a $200 billion-a-year industry feature.

- The Real Reason (That No One Says Out Loud)

Most ESG initiatives threaten the core business model that made these companies rich in the first place.

- Oil companies cannot take climate seriously without admitting their reserves are stranded.

- Fast fashion cannot take human rights seriously without admitting $8 T-shirts are impossible under decent labor laws.

- Tech giants cannot take data privacy seriously without killing behavioral advertising.

- Banks cannot take biodiversity seriously without stopping project finance in the Amazon.

Serious ESG = lower profits or complete business model redesign.

No board will vote for that when shareholders can sue them for breaching fiduciary duty.

The Breakthrough Point (It’s Coming — Just Not from Goodwill)

Change will not come from moral awakening. It will come when three things happen simultaneously:

- Physical climate damages exceed $500 billion annually in insured losses (we are on track for 2027–2029).

- A major sovereign debt crisis hits a country that ignored transition risks (think Italy or Japan).

- Gen-Z + Millennials own >50% of investable assets in the US (projected 2032–2035).

When insurance companies stop insuring coastal real estate, when pension funds blow up because of stranded assets, when the median voter and median investor is someone who was in high school during the 2020 Australia fires — then, and only then, will the cost-benefit equation flip.

Until that moment, most companies will continue to do the absolute minimum required to keep the activists quiet, the regulators at bay, and the ESG ratings agencies happy.

That minimum is now highly sophisticated. The sustainability reports are beautiful. The Net zero targets are scientifically aligned. The TCFD disclosures are exhaustive. The green bonds are oversubscribed.

Everything looks perfect.

That is exactly how you know it isn’t real.

The corporations are not failing at ESG.

They are winning at fake ESG — and the current system rewards them handsomely for it.

The rest of us are the ones failing to change the system fast enough.